India’s 2026 Crypto Tax Guide: Why You Can Lose Money Overall and Still Owe Tax

Crypto taxation in India presents a unique paradox: you can finish the year with a net loss yet still owe tax. Two key provisions drive this outcome:

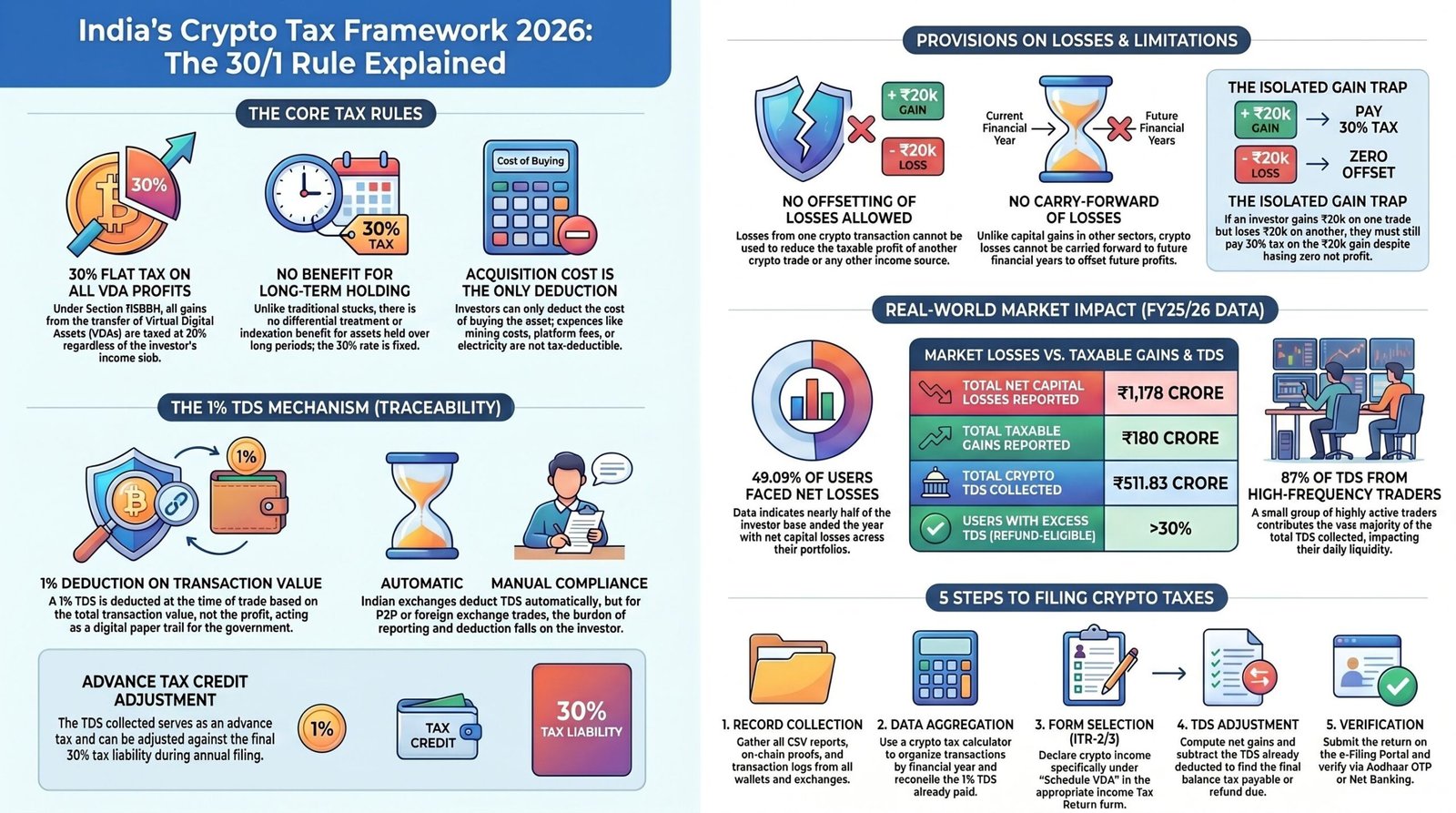

- Section 115BBH taxes each profitable crypto transfer at 30%, with no set-off or carry-forward of losses.

- Section 194S mandates 1% TDS (tax deducted at source) on the transaction value (not on profit) to create a paper trail.

Master these two levers and you’ll understand your real tax and cash-flow drag before you trade—and file without surprises. (1)

Table of Contents

- Introduction

- Legal Framework and Taxation Principles

- Analysis of the 30% Flat Tax Rate

- Understanding the 1% TDS Mechanism

- Provisions on Losses and Their Limitations

- Practical Examples in Crypto Transactions

- Impact of Budget 2026 on Crypto Taxation

- Detailed Process for Filing Crypto Taxes

- Real-World Data and Case Study Insights

- Conclusion and Key Findings

- 2026 Legal and Financial Disclaimer

- Sources

1. Introduction

India’s Virtual Digital Asset (VDA) rules did not lighten in 2026. The Finance Act, 2026:

- Retained the 30% tax on crypto gains under Section 115BBH and the 1% TDS under Section 194S.

- Tightened reporting by introducing new penalties for entities that fail to furnish or misreport crypto-transaction statements.

The playbook to stay compliant is rigorous record-keeping and disciplined cash-flow management, rather than “netting” gains and losses. (2)

Background Note: Many jurisdictions allow loss harvesting or carrying forward losses, but India prioritizes uniform taxation and traceability over such reliefs, making the system predictable yet unforgiving.

2. Legal Framework and Taxation Principles

- What is a VDA?

Section 2(47A) defines a virtual digital asset (crypto, notified NFTs, and other notified digital assets). The government expressly excluded gift cards, reward/mileage points, and certain subscriptions from the VDA definition. (1) - Core tax provision (Section 115BBH):

- Imposes 30% tax on income from the transfer of any VDA.

- Only the cost of acquisition is deductible; platform fees, interest, mining electricity, etc., are not deductible against VDA income.

- No set-off against any other income and no carry-forward of losses. (1)

- Withholding and tracing (Section 194S):

- Requires 1% TDS on the consideration paid to a resident for a VDA transfer, with thresholds and mechanics detailed in CBDT Circular 13/2022.

- The TDS base is the net consideration after excluding GST or other charges levied by the deductor.

(5)

- Filing requirement:

Schedule VDA in ITR-2 (for non-business individuals) or ITR-3 (for business/profession) requires transaction-wise reporting; instructions ask for details of every transfer. (6)

Background Note: India’s philosophy emphasizes uniform taxation and strong traceability over granular reliefs common in securities taxation frameworks.

3. Analysis of the 30% Flat Tax Rate

- Rate and base:

- 30% applies to each transfer’s profit, calculated as sale value minus cost of acquisition.

- Platform fees, interest, mining electricity, and similar expenses are not deductible.

- Cess and surcharge apply separately. (1)

- Scope of “transfer”:

- Applies whether you treat the activity as investment or business.

- Section 115BBH(3) defines “transfer” broadly, covering all dispositions of a VDA. (1)

- Gifts received:

- If you receive VDA without consideration or for inadequate consideration, and the total value exceeds ₹50,000, it’s taxed under Section 56(2)(x) as Income from Other Sources.

- Later disposal still qualifies for 30% taxation under Section 115BBH, with your tax‐paid receipt price becoming your cost of acquisition. (9)

Editorial note: A single special rate simplifies enforcement but removes reliefs investors typically have with traditional securities.

4. Understanding the 1% TDS Mechanism

TDS under Section 194S is not the final tax—it serves as a tracking tool and advance credit.

Key features:

- Trigger: Payment of consideration for a VDA transfer to a resident.

- Rate: 1% on the net consideration (after excluding GST/charges levied by the deductor).

- Thresholds:

- ₹50,000 per financial year for specified persons (certain individuals and Hindu Undivided Families).

- ₹10,000 per financial year for others.

(5)

Who must deduct TDS?

| Platform Type | Deductor | Form Filed / Issued | Citation |

|---|---|---|---|

| Indian centralized exchanges | Exchange | Form 26QF | (11) |

| Peer-to-peer (P2P) transactions | Buyer (specified persons) | Form 26QE (challan-cum-statement) and issue Form 16E | (13) |

| Crypto-to-crypto swaps | Exchange (in kind) | 1% withheld on both legs, converted to INR deposit | (11) |

- Residency check: If the payee is a non-resident, Section 195 may apply instead; professional advice is advised. (5)

Takeaway:

- TDS can exceed your final liability and requires a refund claim when your actual tax is lower.

- It creates a year-round cash-flow drag (roughly 1% of gross sell value).

5. Provisions on Losses and Their Limitations

- No set-off: VDA losses cannot be offset against VDA gains or any other income. (1)

- No carry-forward: Unused VDA losses cannot be carried into future years. (1)

- Gifts: If taxed under Section 56(2)(x) on receipt, that amount becomes your cost of acquisition for future 115BBH calculations. (9)

Implication: You can be net-negative on the year and still owe tax on each profitable sell.

6. Practical Examples in Crypto Transactions

Note: Cess and surcharge are ignored for simplicity. TDS is calculated on “net consideration” (excluding platform charges/GST if levied by the deductor).

| Example | Transaction Details | Profit/Loss | Tax @ 30% | TDS @ 1% | Net Payable |

|---|---|---|---|---|---|

| A | Buy ₹100,000 → Sell ₹120,000 | ₹20,000 gain | ₹6,000 | ₹1,200 | ₹6,000 − ₹1,200 = ₹4,800 (1) |

| B | Trade 1: +₹20,000; Trade 2: −₹20,000 | Net zero | ₹6,000 on gain | 1% on each sell value (~₹1,200 + ₹800) | Loss cannot offset gain; tax still due on ₹20,000 gain (1) |

| C | Swap ETH → SOL worth ₹50,000 | Depends on cost basis | Pay 30% on any gain vs ETH cost | 1% withheld in kind | Later compute and pay on gains (11) |

| D | P2P buy from resident: USDT ₹30,000 | N/A | N/A | ₹300 (1%) | Deductor (buyer) must file 26QE and issue 16E (11) |

Rule of thumb for active traders: Expect a cash drag of roughly 1% of gross sell value or swap legs; refunds arrive only after assessment if your final 30% tax liability is lower.

7. Impact of Budget 2026 on Crypto Taxation

- Core rates unchanged:

- 30% under Section 115BBH

- 1% TDS under Section 194S (24)

- New platform-level penalties (effective April 1, 2026):

- ₹200 per day for non-furnishing of crypto-asset statements.

- ₹50,000 for inaccurate particulars or failure to correct under new Section 446 of the Income-tax Act, 2025 (as amended).

These penalties target reporting entities, not retail holders. (2)

- Enactment status: Finance Act, 2026 received Presidential assent on March 30, 2026. (26)

Editorial note: Budget 2026 doubles down on enforcement rather than granting reliefs (such as loss set-off or lower TDS) that the industry had lobbied for.

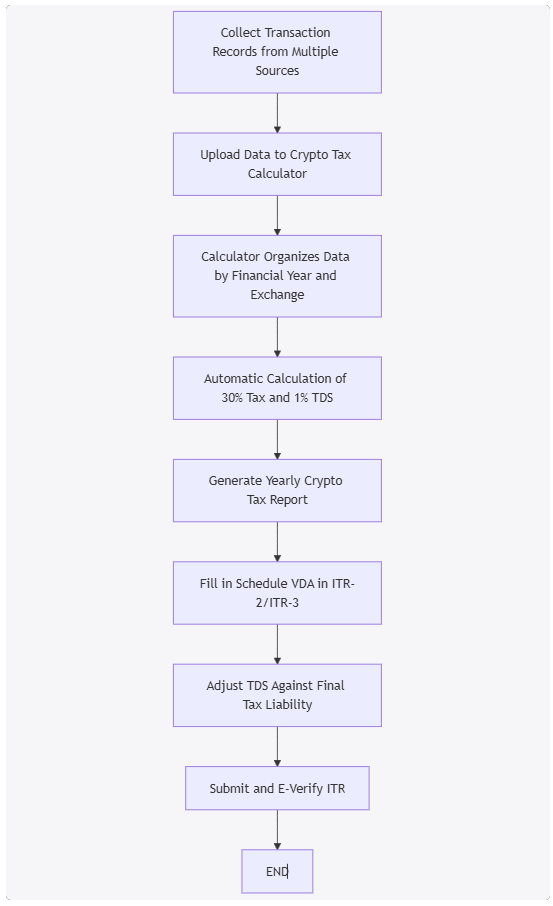

8. Detailed Process for Filing Crypto Taxes

- Collect records

- Exchange trade history (CSV), on-chain TXIDs, wallet addresses, P2P invoices, and any Form 16E/26QE issued or received.

- Cross-check Form 26AS/AIS for TDS under Section 194S. (27)

- Use a crypto tax calculator (optional but practical)

- Tools consolidate exchange and wallet data, compute per-trade profit/loss under Section 115BBH, and reconcile TDS credits for Schedule VDA. (28)

- Choose the right ITR and fill Schedule VDA

- ITR-2 (no business income) or ITR-3 (business/profession).

- Schedule VDA requires every transfer as a separate transaction. (6)

- Reconcile TDS

- Exchange-deducted TDS (Form 26QF) should auto-appear in Form 26AS/AIS.

- For your own P2P deductions as a specified person, ensure Form 26QE was filed and Form 16E issued; claim credit in your ITR. (11)

- File and e-verify

- File by due dates. Under AY 2026-27 onward, general late-filing fees apply as per the Finance Act, 2026 (₹1,000 / ₹5,000). (2)

Do-this-now checklist:

- Enable monthly exports on every exchange; tag P2P buys; keep TXIDs.

- If you are a specified person buying on P2P, deduct 1% via Form 26QE and issue Form 16E on time.

- Prior to filing, match your tool’s sell totals with the 26AS VDA TDS entries; address gaps to avoid “defective return” notices. (0)

9. Real-World Data and Case Study Insights

| Metric | Value / Insight | Source |

|---|---|---|

| FY25 profit/loss mix | KoinX’s FY25 cohort showed net capital losses of ~₹1,178 crore and taxable gains of ~₹180 crore. | 33 |

| Offshore trading volume | 72% of trading volumes shifted offshore in FY25. | 33 |

| TDS collections | VDA TDS rose ~41% to ₹511.83 crore in FY25 (implying >₹51,000 crore of taxable turnover). | 34 |

| State-wise leader | Maharashtra and Karnataka led in VDA TDS collections. | 34 |

Implication: The 1% TDS liquidity cost is material for high-frequency traders—refunds arrive later, but the drag is real during the year.

Edge debate—derivatives:

Industry commentary suggests that cash-settled crypto futures/options may not be VDAs and could be taxed as (speculative) business income rather than under Section 115BBH. No CBDT-level clarification exists yet. If you trade derivatives, document your position and consult a tax professional. (35)

10. Conclusion and Key Findings

- 30% on each profitable transfer, with cost-only deduction and no loss set-off or carry-forward. (1)

- 1% TDS is on value (net of platform charges), not profit; thresholds are ₹50,000 / ₹10,000 depending on taxpayer category; exchanges and P2P participants have distinct responsibilities. (11)

- Budget 2026 maintained rates and added penalties to enforce cleaner reporting at the platform level. (2)

- Filing in 2026 requires accurate Schedule VDA, thorough TDS reconciliation (26QF/26QE/16E), and timely e-verification. (6)

Light take: In India, crypto tax planning centers on trade-by-trade hygiene and cash-flow discipline, not classic tax-loss harvesting.

2026 Legal and Financial Disclaimer

This guide is for general information and education on India’s crypto tax regime as of April 30, 2026. It is not legal, tax, or investment advice. Laws, circulars, forms, and portal behavior can change and may apply differently to your facts (e.g., residency, source of income, business vs. investment treatment, and derivative products). Consult a qualified tax professional before acting. Indi Crypto and the author assume no liability for decisions made based on this guide.

Sources:

- Income-tax Act: Section 115BBH (Tax on income from virtual digital asset) + Section 2(47A) (VDA definition). Official PDF: https://incometaxindia.gov.in/documents/20117/11892059/Section-%20-115BBH_en_310100.pdf (1)

- CBDT Circular No. 13/2022: TDS under 194S; exchange/P2P mechanics; crypto-to-crypto; net consideration. https://incometaxindia.gov.in/Communications/Circular/Circular-No-13-2022.pdf (11)

- Section 194S bare text (Payment on transfer of virtual digital asset). https://incometaxindia.gov.in/Acts/Income-tax%20Act%2C%201961/2025/102120000000091302.htm (5)

- CBDT Notifications on exclusions and NFT specifications (Nos. 74/2022 and 75/2022). https://incometaxindia.gov.in/communications/notification/notification-no-74-2022.pdf; https://incometaxindia.gov.in/communications/notification/notification-no-75-2022.pdf (43)

- ITR-2 FAQ and notification on Schedule VDA details. https://www.incometax.gov.in/iec/foportal/help/FileITR-2Online-FAQ; Notification No. 46/2026 on Schedule VDA tables (6)

- TDS forms for 194S (26QE challan-cum-statement; 16E certificate) and compliance FAQs/Calendar. https://incometaxindia.gov.in/Rules/Income-Tax%20Rules/103120000000009477.htm; https://traces61contents.tdscpc.gov.in/en/faq-taxpayer-26QE.html (46)

- Finance Bill/Act 2026: Penalties for crypto-asset statement failures; ₹200/day and ₹50,000 for inaccuracy. https://www.indiabudget.gov.in/doc/Finance_Bill.pdf (2)

- Budget 2026 media explainers on unchanged rates/new penalties. Examples: Economic Times; Fortune India; Moneycontrol. (24)

- KoinX FY25 coverage (offshore share; loss/gain mix) via Moneycontrol; TDS statewise data via CAclubIndia. https://www.moneycontrol.com/news/business/over-72-of-indian-crypto-trading-volumes-went-to-offshore-exchanges-in-fy25-koinx-report-13797772.html; https://www.caclubindia.com/news/maharashtra-leads-crypto-tds-collections-as-vda-tax-revenues-jump-41-percent-in-fy25-25991.asp (33)

- Big-4/industry explainers summarising 115BBH/194S frameworks (e.g., PwC India). https://www.pwc.in/tax-knowledge-hub/taxation-framework-of-virtual-digital-assets.html (50)

- Industry debate (derivatives): BDO/ET coverage on unresolved treatment for crypto F&O. https://economictimes.indiatimes.com/wealth/tax/budget-2024-why-crypto-fo-investors-are-happy-no-stt-no-tds-no-30-tax/articleshow/112126004.cms (35)