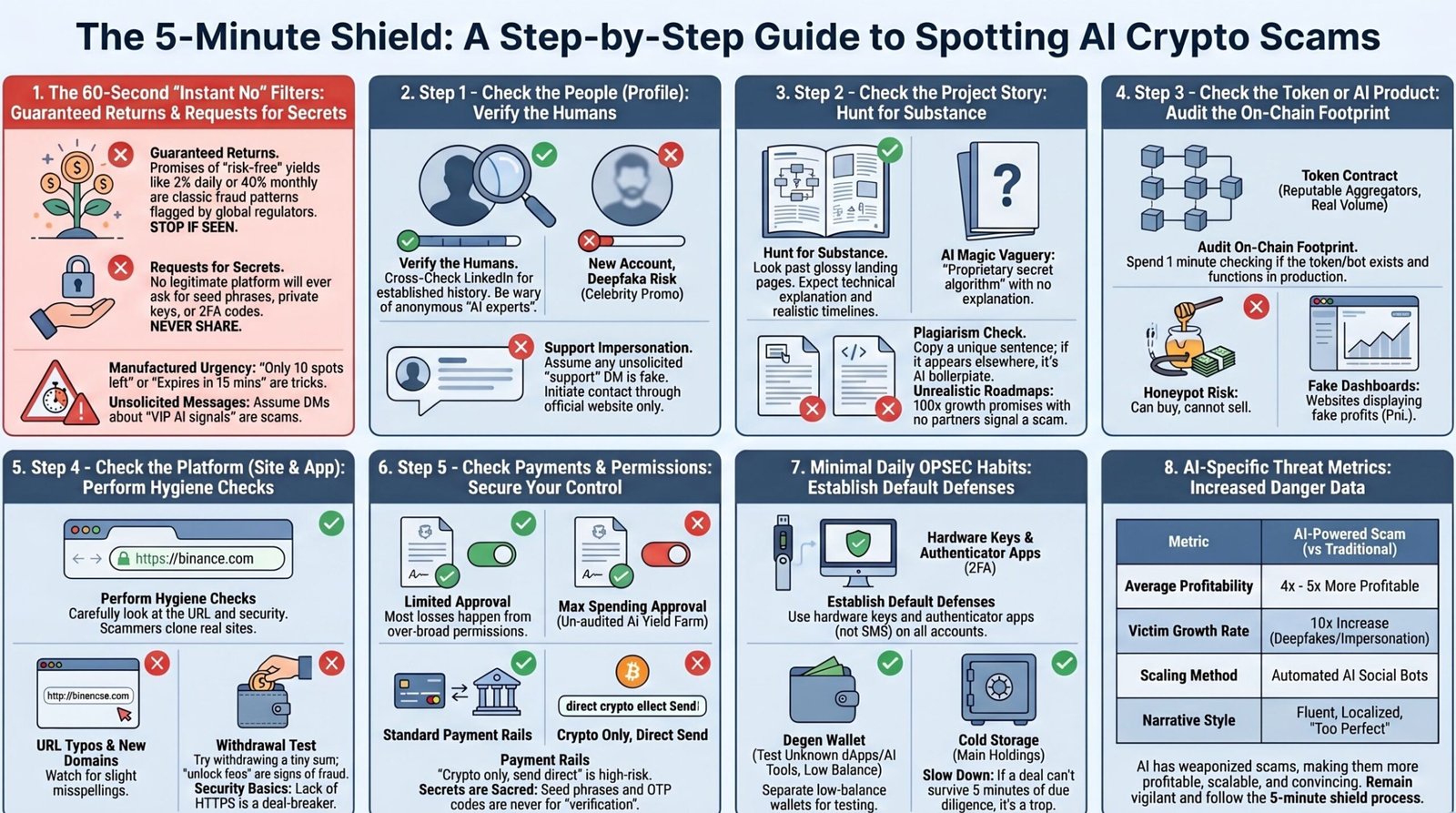

Scammers just stole $17 billion from crypto investors in 2025 alone — and artificial intelligence is the reason it’s harder than ever to tell the difference between a legitimate project and a sophisticated fraud.

AI hasn’t invented new scam types. It has weaponised old ones, making fake teams, fake bots, fake celebrity endorsements, and fake trading platforms look indistinguishable from the real thing. The good news? You can still spot the warning signs — if you know what to look for and take five focused minutes before you send a single cent.

This is Indi Crypto’s battle-tested 5-minute checklist. Bookmark it. Run it every time.

The 60-Second “Instant No” Test

Before anything else, run this filter. If you see any of the following, stop immediately — you do not need more research.

- Guaranteed or “risk-free” returns. Promises like “2% per day, “40% monthly guaranteed”, or “AI that never loses” are fraud patterns flagged by the CFTC, FINRA, and NASAA.

- Requests for your seed phrase, private keys, or 2FA codes. No legitimate exchange, wallet, or trading bot will ever need these — full stop.

- Extreme urgency and scarcity. “Only 10 spots left”, “offer expires in 15 minutes”, “deposit now or miss the pump” are pressure tactics designed to switch off your critical thinking.

- They contacted you first. Unsolicited DMs on WhatsApp, Telegram, X, or Instagram about a “special AI opportunity” or “VIP signals group” are a classic entry point for scammers.

- Fees to withdraw your own money. If a platform demands a “tax”, “unlock fee”, or “security deposit” before releasing your funds, you are almost certainly inside a scam.

- Requests for remote access or screen-sharing. “Support” asking to control your phone or PC to “help” with a wallet is a direct path to a drained account.

Hit any of these? Close the chat, block the contact, and report it. No one is smart enough to outplay a professional scam operation — and trying costs you.

Step 1: Verify the People Behind the Project

AI has made fake humans terrifyingly convincing. Deepfake videos, AI-generated profile photos, and cloned voices are all standard tools in large-scale scam operations today. Your first job is to sanity-check the people.

Founders and advisors: Look them up on LinkedIn and other professional platforms. Do they have years of verifiable history, mutual connections, and previous roles you can actually confirm — or were their profiles created in the last few months?

Deepfake risk: Be sceptical of any video featuring a celebrity or CEO — Elon Musk, CZ, Vitalik, or prominent executives — promoting an “official AI coin” or offering to double your Bitcoin. Deepfake promo videos are now a standard, scalable tool in high-value scam operations, and AI-linked fraud has been measured as over four times more profitable than traditional schemes.

Support impersonation: On Telegram, Discord, and WhatsApp, assume any DM from “exchange support” is fake unless you personally initiated contact through the platform’s official website or app.

If the humans don’t check out, the project doesn’t deserve another minute of your time.

Step 2: Analyse the Project Story

Thanks to AI, anyone can generate a glossy whitepaper, a professional website, and a roadmap full of impressive-sounding milestones in an afternoon. You are hunting for substance behind the polish. Ask three quick questions:

Is the “AI magic” actually explained? Terms like “proprietary AI”, “secret algorithm”, and “can’t-lose strategy” with no technical detail, no data source, and no model description are precisely the kind of hype regulators warn about.

Is the content original? Copy a distinctive sentence from the whitepaper or website, paste it into Google, and see what comes up. If identical paragraphs appear across multiple unrelated projects, you may be looking at AI-generated boilerplate or plagiarism.

Is the roadmap grounded in reality? Promises of Tier-1 CEX listings, multi-chain deployment, and 100x growth within weeks — with no real funding, no verifiable team, and no existing partners — are classic red flags.

Real builders are specific. They are boringly honest about risks and transparent about what they cannot do yet.

Step 3: Check the Token or AI Bot On-Chain

If the people and story still hold up, take another 60–90 seconds to verify what actually exists on-chain and in production.

Listings and liquidity. Is the token listed on reputable aggregators like CoinGecko or CoinMarketCap with real trading volume and a meaningful history — or is it only available through a random DEX link someone sent you in a group chat?

Smart-contract basics. On a block explorer like Etherscan or BscScan, check whether the contract is verified, whether trading is open to all users, and whether fees or tax parameters are set suspiciously high.

Honeypot check. For meme-style AI coins launched on DEXs, run a dedicated honeypot checker tool and test with a tiny buy and sell from a fresh wallet. If you can buy but not sell, leave immediately.

Is there a working product? Many “AI trading bots” are nothing more than polished dashboards that accept deposits and display fabricated profit-and-loss numbers. No live app, no verifiable API connection to a real exchange, no audited smart contract — treat it as a marketing site, not an investment. If there is no product, you are not investing early. You are the product.

Step 4: Inspect the Platform (Site or App)

AI has made it cheap and fast to clone the look, feel, and branding of well-known exchanges and wallets. A quick platform check takes under a minute and can save you from handing your credentials to a fake Coinbase or Binance.

URL and domain age. Check the address letter by letter. Scammers register domains like coinbsae.com instead of coinbase.com, or use “brand-support” clones registered only weeks ago.

Security basics. No HTTPS padlock, certificate warnings, strange redirects, or a login screen asking for your seed phrase are immediate deal-breakers.

Test withdrawals first. On any unfamiliar platform, deposit a minimal amount and immediately attempt to withdraw it. Legitimate platforms make withdrawal straightforward. If the platform suddenly invents new fees, taxes, or “security verifications” the moment you try to withdraw, treat it as a confirmed scam.

Step 5: Check Payments and Wallet Permissions

Most serious financial losses happen in one of two ways: surrendering secrets or granting over-broad smart-contract permissions to a malicious address.

Secrets are sacred. Seed phrases, private keys, SMS one-time codes, and authenticator codes are never required to “verify” your account, “unlock” a reward, or “secure” your funds. Any request for these is fraud — without exception.

Wallet approvals. If an “AI yield farm” or “AI rebalancer” asks for a max spending approval on your stablecoins or established tokens, treat it the same as giving unlimited signing authority on your bank account. Only grant max approvals to audited, battle-tested protocols with years of track record — never to a project you found through a group chat link.

Payment methods. Reputable platforms support multiple payment rails, publish clear terms and conditions, and have identifiable legal entities. “Crypto only, send directly to this wallet address, no invoice, no company name” is high-risk territory.

If you hesitate even slightly while signing a transaction, that hesitation is your signal to stop and re-read exactly what you are authorising.

AI-Specific Red Flags to Watch in 2026

AI has not created new categories of fraud. It has made every old playbook dramatically more scalable and convincing. Here is what is growing fastest right now:

Deepfake endorsements. Live-streamed “giveaways” featuring deepfaked CEOs on YouTube, TikTok, and X have become routine. AI-linked scam operations are documented as generating over four times the revenue per victim compared to non-AI scams, driven largely by the credibility that realistic video lends.

AI-scaled social bots. Thousands of AI-written comments and direct messages — fluent in local languages and slang — can make a completely fake project look like the hottest opportunity in the market overnight. Chainalysis has documented a sharp rise in AI-driven impersonation and pig-butchering operations in its 2026 Crime Report.

Fake “investment education foundations”. Regulators like NASAA have documented schemes where “foundations” use WhatsApp groups, fabricated student success stories, and a “proprietary AI bot” hosted on a controlled exchange. Victims are given free tokens to build confidence, then encouraged to deposit real funds that are later blocked.

AI customer support impersonation. Voice-cloned “agents” and AI chatbots now impersonate banks, exchanges, and wallet providers, contacting users about “suspicious activity” or “account verification” with the goal of moving funds or extracting credentials.

The pattern is always the same: emotional pressure, manufactured urgency, and the promise that AI removes all risk from investing.

Daily Security Habits for the AI Era

You do not need to be paranoid. You do need updated habits. With average losses per victim rising sharply and AI making scams harder to detect on first impression, basic defensive routines are now non-negotiable.

- Treat “too good to be true” as a hard no — especially when AI is cited as the reason there is no risk.

- Use hardware wallets for meaningful holdings and enable 2FA or passkeys on all exchanges and email accounts, preferably via an authenticator app rather than SMS.

- Maintain a dedicated “degen” wallet with minimal funds for testing unknown dApps, AI bots, and new protocols — keep your core holdings in cold or well-segmented storage.

- Slow down under pressure. Scammers live off urgency and FOMO. If a deal cannot survive five minutes of this checklist, it is not an investment. It is a trap.

The bottom line: AI has made scams smarter, but it has also made verification tools, on-chain explorers, and credible information more accessible than ever. Make “verify first, invest later” your default setting — every single time.

Frequently Asked Questions

What are the most common AI crypto scams in 2026?

The most prevalent include AI trading bot frauds (fake dashboards showing fabricated returns), deepfake celebrity endorsements on YouTube and TikTok, pig-butchering romance scams using AI personas, and AI-impersonated customer support agents.

How do I know if an AI trading bot is a scam?

Check for an audited smart contract, a verifiable API connection to a real exchange, a publicly identifiable team, and a functioning withdrawal process. If any of these are missing — especially if withdrawals require extra fees — treat it as a scam.

What should I do if I’ve been scammed in crypto?

Stop sending money immediately, document everything (screenshots, wallet addresses, transaction IDs), report to your national financial regulator (e.g., CFTC in the US, FCA in the UK, BaFin in Germany), and report the wallet address to Chainalysis or your exchange’s fraud team.

Is it safe to use AI tools for crypto trading?

Legitimate AI tools exist and are used by professional traders. The key difference is that real platforms are audited, registered, transparent about risk, and do not guarantee returns. Any AI tool guaranteeing profits is either misleading or fraudulent.

How do deepfake crypto scams work?

Scammers generate realistic video or audio of celebrities, executives, or regulators using AI synthesis tools, then broadcast these as “live” events on social platforms, promoting fake coin launches or doubling schemes. The videos are often indistinguishable from genuine footage at first glance.

Sources

- Chainalysis – 2026 Crypto Crime Report: Scams [chainalysis.com/blog/crypto-scams-2026]

- Chainalysis – AI-Powered Crypto Scams: How AI Is Being Used for Fraud [chainalysis.com]

- Crypto.com University – Understanding AI Scams in Cryptocurrency [crypto.com]

- CFTC – Customer Advisory on AI-Themed Trading and Crypto Schemes [cftc.gov]

- FINRA – Artificial Intelligence and Investment Fraud [finra.org]

- NASAA – Elaborate Cryptocurrency Scams Involving AI Bots [nasaa.org]

- Quest CE – Regulators Caution Investors on the Promise of AI [questce.com]

- Walbi – AI Coin Scams & How to Spot Them [walbi.com]

- Coin.space – AI-Powered Crypto Scams: Real Examples 2026 [coin.space]

- Ohio Consumer Protection – AI-Powered Scams and How to Protect Yourself [com.ohio.gov]

- ESMA – Online Financial Frauds and Scams in an AI World [esma.europa.eu]

- Pronto Software – How to Protect Yourself Against AI-Powered Scams [pronto.net]

⚠️ Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Always conduct your own due diligence before investing.